Overall air traffic was up from November while the average airfare decreased slightly. The preliminary true O&D level data released by FlightBI this week shows that US domestic passenger volume increased from November 2022 to December 2022 by 2% and the average domestic airfare decreased by 1%.

Volume Trend

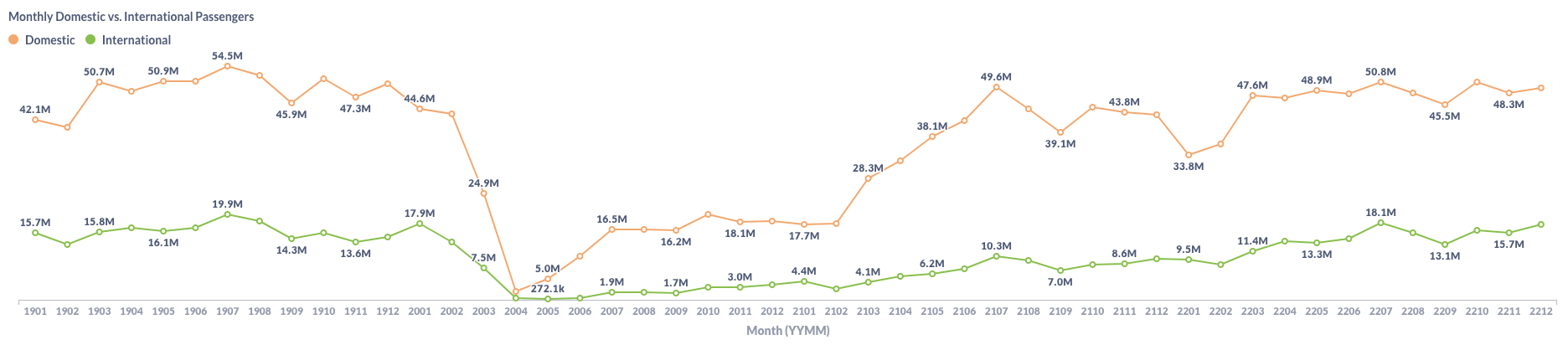

US domestic traffic by true O&D increased from 48.3 million passengers in November to 49.4 million in December, which is lower than the pre-pandemic level of 50.3 million in December 2019. The US international traffic increased more, from 15.7 million in November to 17.7 million in December.

Figure 1: US Domestic and International Air Traffic by Month

Airfare Trend

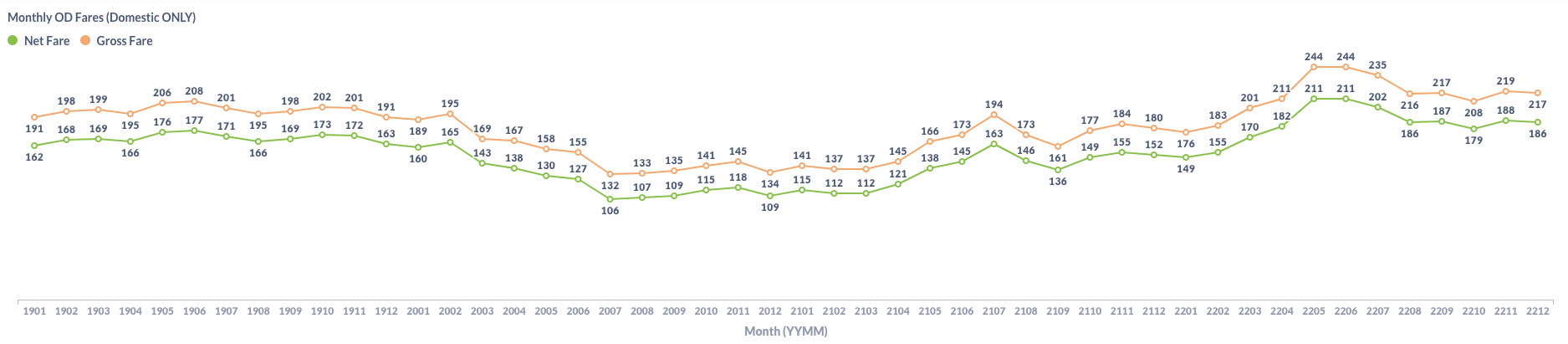

The average domestic gross fare was down from $219 in November to $217 in December. The average net fare also decreased from $188 to $186 over the same period.

Figure 2: US Domestic Average Airfare by Month

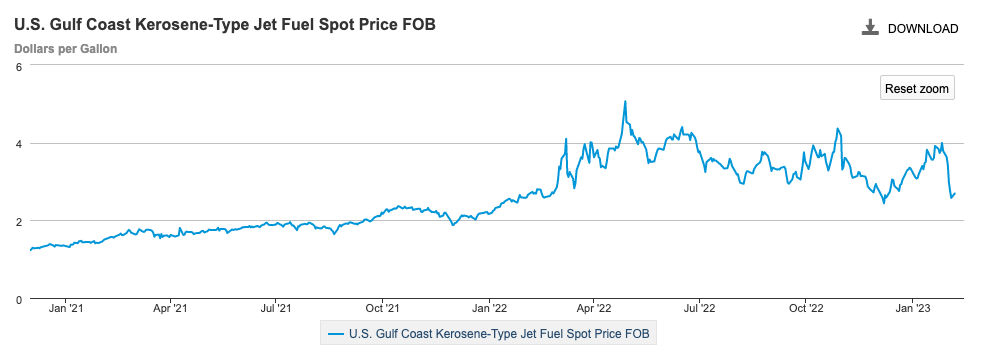

Airfare decreased slightly because jet fuel price dropped from November to the beginning of December 2022, as shown in the chart below provided by EIA. Since the jet fuel price increased again in December 2022 and January 2023, we expect that the average airfare will stay at this level for at least another month.

Figure 3: US Jet Fuel Price

Load Factor Trend

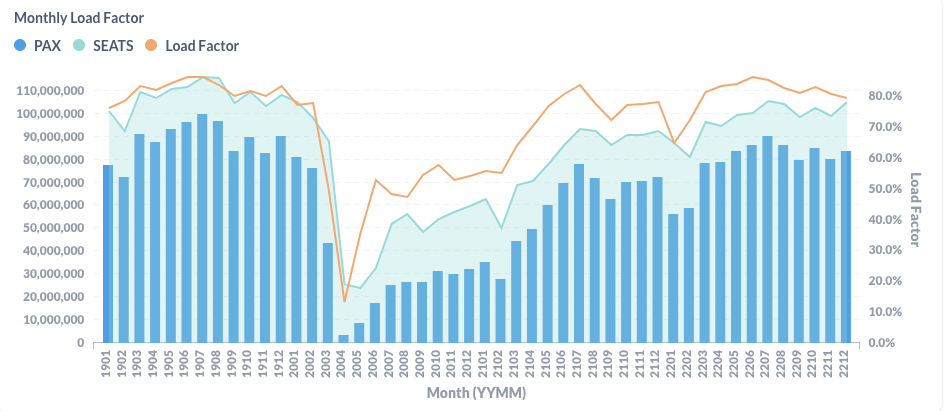

The average load factor in December was 79.4%, further deteriorated from previous two months. As shown in Figure 4 below, both traffic and capacity increased in December, but the traffic growth was slower than the capacity increase.

Figure 4: US Airlines’ Average Load Factor by Month

Month Over Month Comparison

From November to December, Allegiant(G4) gained 14.4% of traffic per day. Hawaiian(HA), Frontier(F4) and United(UA) also had some growth. American(AA) and JetBlue(B6) barely changed. But Delta(DL), Spirit(NK) and Alaska(AS) carried fewer passengers per day in December than the previous month.

Figure 5: Air Traffic by Dominant Marketing Airlines in December 2022 (Current) vs. November 2022 (Previous)

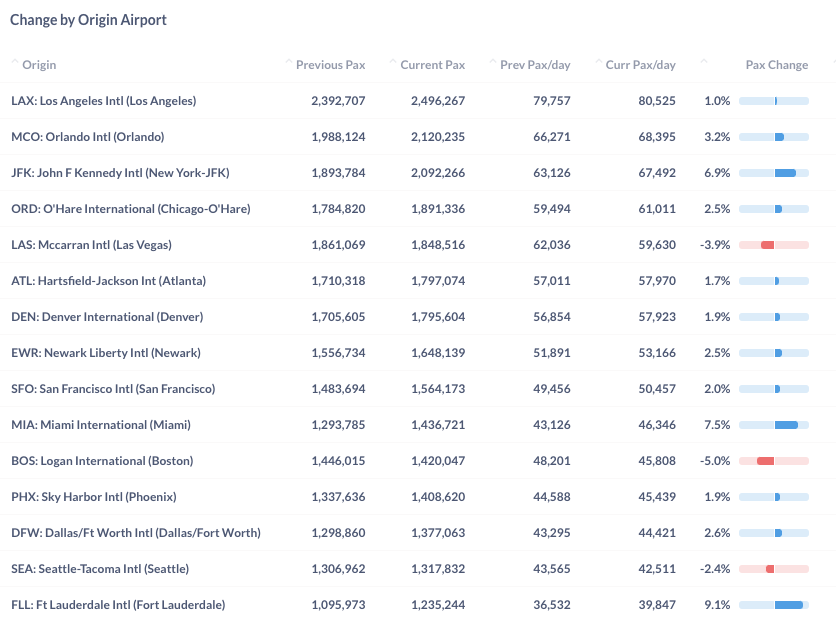

Most top airports had more traffic in December than in November. Three largest airports in Florida – Ft. Lauderdale(FLL), Miami(MIA) and Orlando (MCO) achieved the most growth because those are good Christmas destinations. Boston (BOS) and Las Vegas (LAS) continued their decline and had a 5.0% and 3.9% decrease, respectively, from November.

Figure 6: Air Traffic by Top Origin Airports in December 2022 (Current) vs. November 2022 (Previous)

Year Over Year Comparison

Compared to the same month last year, all major US airlines had achieved positive growth. Frontier(F9) and Spirit(NK) led with a year-over-year growth rate of 32.9% and 30.9%, respectively. But the largest legacy carrier American(AA) only grew its daily traffic by 6.3%.

Figure 7: Air Traffic by Dominant Marketing Airlines in December 2022 (Current) vs. December 2021 (Previous)

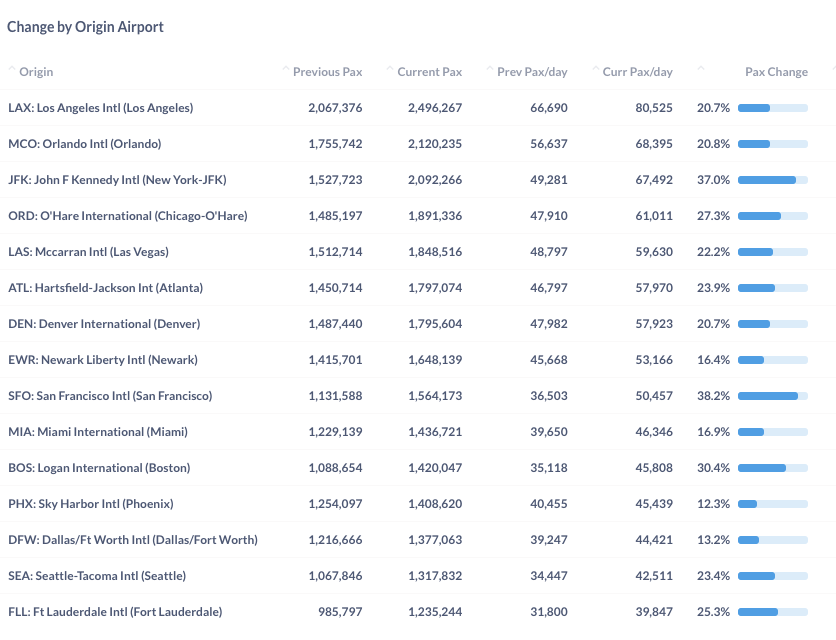

Growth by top airports is still very good. All top airport achieved double-digit growth from December 2021 to December 2022. San Francisco (SFO) airport and New York (JFK) airport led the year-over-year growth with 38.2% and 37.0%.

Figure 8: Air Traffic by Top Origin Airport in December 2022 (Current) vs. December 2021 (Previous)

For more granular traffic and fare information by route and airline, please get in touch with service@flightbi.com or request a demo of Fligence USOD.